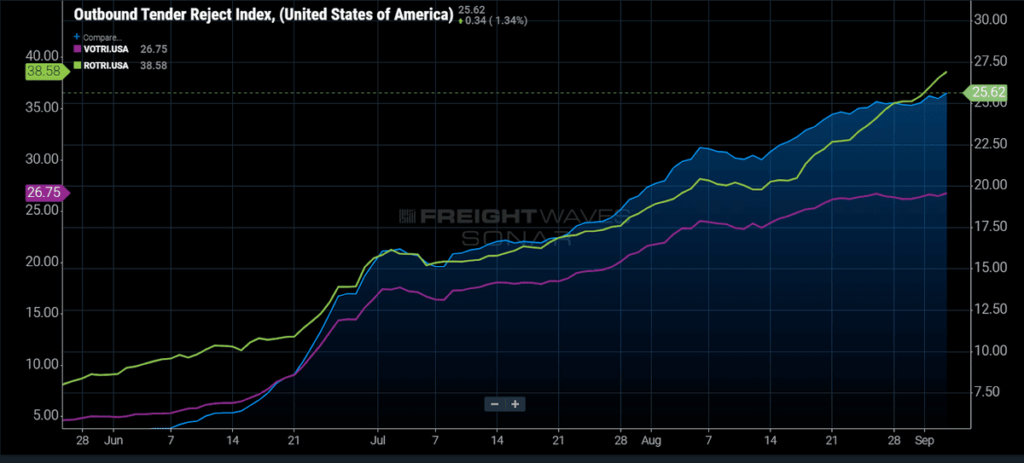

What are Outbound Tender Volumes Saying about the Market this Week?

The Outbound Tender Volume Index (OTVI) climbed another 1.4% last week to a new all-time high of 16,053. OTVI has posted a string of consecutive all-time highs for many weeks now. It is important to note that OTVI does include rejected contract load tenders, so the true organic growth of load volumes is significantly lower than the indexed reading as explained later. However, this does not mean the index is not directionally accurate or not indicative of the overall strength in the freight market. However, the rate of volume acceleration has begun to slow.

To account for the high level of rejected tenders in SONAR’s Outbound Tender Volume Index, a new metric, a proxy index for accepted tenders, has been calculated. Using this correction, volumes are running about 19% higher year-over-year and are at a three-year high. Carriers are rejecting one in four contracted load tenders, and spot rates have pushed north of $2.75 per mile on a national basis.

The extremely high level of tender rejections is distorting the true volume level. To account for that, one can use this simple formula to calculate the indexed level of accepted tenders as a proxy (note this is not the actual number of accepted tenders, which is proprietary): OTVI* (1-OTRI) for any given day. We also note that we chose to use last Thursday’s (September 3) readings to remove Labor Day-related distortions.

16,128* (1 – .25) = 12,096 accepted load proxy index for September 2, 2020

10,660* (1 – .046) = 10,127 accepted load proxy index for September 2, 2019

Using this metric to control for the high level of rejected tenders allows us to get a more accurate understanding of the true demand level. This does not mean demand is not at a historically high level – it is. With this metric, trucking volumes (van, reefer, flatbed) are running up over 19% year-over-year.