Shippers hoping for trucking rate relief in 2022 are going to be severely disappointed.

The trucking freight market is one of the most volatile markets on the planet, especially since 2014. What is causing these massive swings? Supply and demand, naturally.

If you really want to understand the market’s rate direction, you must understand how supply and demand is structured. I often hear people that speak of supply (capacity) or demand (freight volume) refer to either one as if that explains pricing alone, when in practice, you must understand how each dynamic moves separately.

Before we talk about 2022, let’s give a quick primer on how supply and demand work in trucking.

Demand: This factor is pretty straight forward. Demand is a reflection of the total volume of trucking freight transactions across the market. If the physical economy (retail, CPG, manufacturing) is doing well, you have more freight transactions. The hotter the consumption of physical goods, the more freight gets shipped.

What should you track to know how healthy each dynamic is? Think CIG – consumer, industrial and government.

Consumer – Consumer spending and sentiment

Industrial – PMI (Purchase Managers Index)

Government – Federal spending (or stimulus programs) on physical infrastructure and defense spending can help you get a sense for the direction of how the government is driving freight demand.

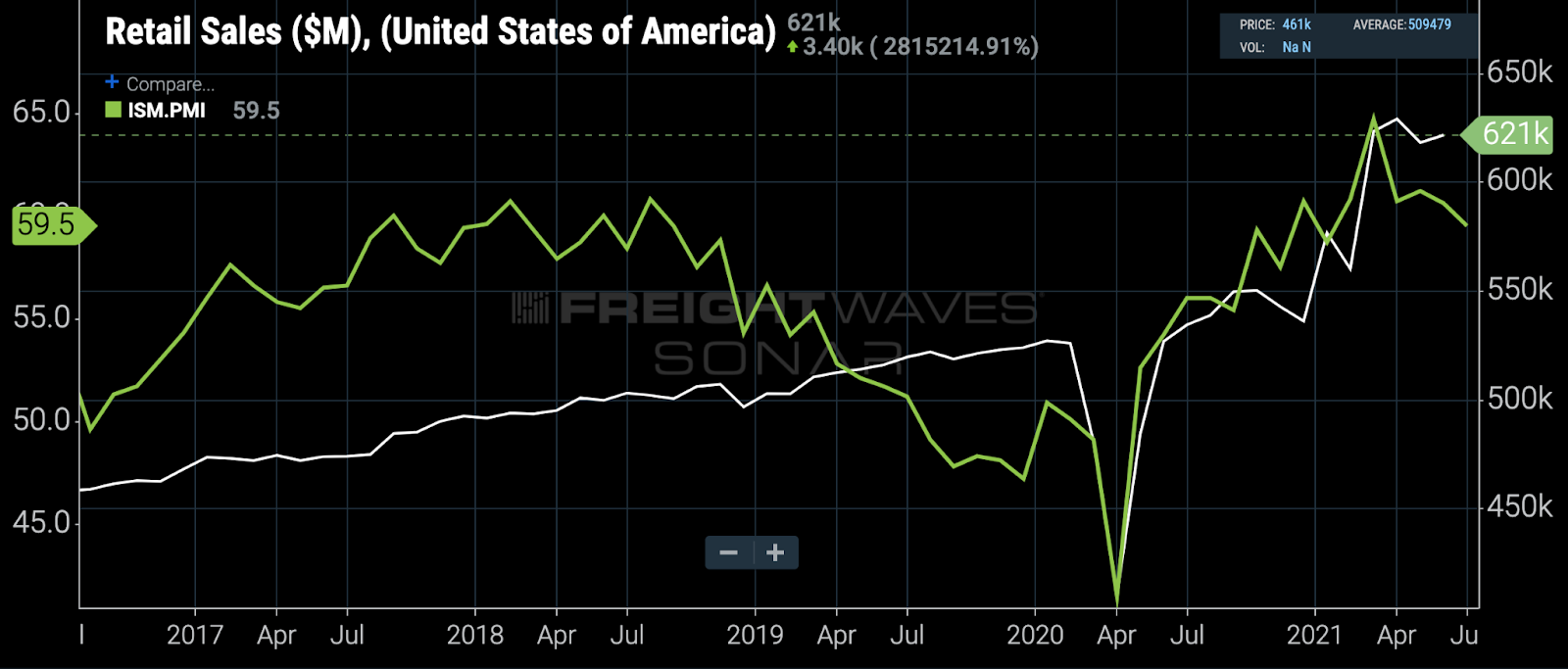

(Retail sales [white] and the Purchasing Managers Index [green] remain very strong. Chart: FreightWaves SONAR)

Supply: This factor is more nuanced and tends to be a combination of physical truck assets in the market and truck drivers willing to drive those trucks.

Truck production tends to be easier to get data on (there are only four major Class 8 OEMs in North America) and they regularly publish data. So we can see how new truck orders are trending. One note of caution is that new truck orders tend to be a lagging indicator and largely driven by the health of trucking spot rates. If trucking spot rates are falling fast, new truck orders will tend to slow about two months later. If trucking spot rates accelerate, you will see orders do the same, usually two months later as well. One thing to keep in mind is that new truck orders do not mean new truck deliveries, just an order that is placed in the market. It can take the truck manufacturers months or even over a year to deliver those orders. But the direction of new truck orders is usually a good indicator of whether capacity is growing or shrinking.

But more importantly, the key statistic to watch is the supply of truck drivers that are willing to drive trucks. The word “driver shortage” is usually a reflection of the number of trucks that exist in the market that do not have a driver to drive them. Remember, a truck doesn’t drive itself (yet). You need a driver.

(As an aside, you can have a capacity glut, while carriers experience a “driver shortage.” This is the worst kind of market. Carriers don’t have enough drivers to drive the trucks that they own, while there is too much capacity on the market to haul the amount of freight. Rates become depressed as carriers aggressively undercut one another hoping to move loads. Meanwhile, the carriers also have trucks that are effectively dead assets and sitting against a fence, costing money, but not generating any kind of revenue. This happened in 2019 and resulted in a bloodbath and the highest number of trucking bankruptcies since the Great Recession).

To understand the number of drivers in the market, we need to track truck driver employment data and the number of owner-operators in the market. Since truck driving employee jobs tend to be jobs of last resort, fewer people apply for truck driving employment jobs, when alternative work exists. Think of jobs in manufacturing, construction, warehousing, fast food, and big box retail as competing sectors for truck driving jobs. If those competing markets are on-fire and demand for labor is high, fewer people will seek trucking jobs.

(Trucking employment still hasn’t retaken the 2018 or 2019 peaks, even though volume is higher. Chart: FreightWaves SONAR).

One other factor in this equation is that when the spot market is really good and freight volume is really high, it becomes incredibly easy to run your own trucking business. Experienced drivers will open their own trucking business, leaving the fleet that employs them. They will seek out loads through a network of freight brokers and load boards and may over time grow their company and employ other drivers.

This is what happened in 2018, when spot rates were at all-time highs. We saw a lot of employees leave their fleet jobs to start their own trucking businesses. They left the carrier they worked for with an “unseated truck,” while also flooding the market with additional capacity.

So where are we now?

(Truckload spot rates [in white] have been putting upward pressure on contract rates [green] for a year now, but the fundamental supply-demand dynamics have not changed yet. Chart: FreightWaves SONAR)

We have record demand in the freight market. The volume of loads in 2021 has kept the trucking industry busy and has provided support for freight rates. With consumer spending at record levels and consumer balance sheets very healthy with money on the sidelines, there are no near-term concerns that consumer freight demand will taper.

Industrial demand is also coming online as companies try to recover from supply chain issues. Companies that simplified their supply chain with fewer sources have been hurt and are now investing in new suppliers and even building their own manufacturing. Much of the industrial demand has been caused by consumer consumption and a lack of inventory. Consumer demand is the “pull” on the industrial economy, or at least it had been.

Now there is one big factor that is new to the market – government spending. And yes, while government spending has been accelerating for decades, much of this spending was tied to things other than physical goods.

The $1 trillion infrastructure bill moving through Congress is mostly about physical goods. Roads, bridges, airports, ports, rail yards, etc. – all have physical elements (concrete, steel, lumber, building materials, etc). All of these things have to be trucked around – i.e. more freight.

While the details are still not clear, one thing about government spending that has proven true – Congress will ensure much of the product and material sourcing for infrastructure takes place in the domestic market and will be distributed so that almost every Congressional district becomes a winner.

More importantly, the bigger impact to the infrastructure bill will be felt on the supply side, particularly for employee drivers. Domestic manufacturing is about to get a massive boost from the infrastructure package and this will mean that the industrial sector will be looking for workers and paying higher wages to attract them. Construction of these new infrastructure projects will also require physical labor, which will also compete for labor with trucking. Add warehousing to store these goods and new job sites and you can imagine just how difficult it will be for trucking fleets to compete for labor.

The upside is that we may enter into a trucking rate and demand supercycle that is driven by a manufacturing renaissance, better infrastructure, and tighter control on capacity growth. While fleet executives will struggle to figure out how to recruit and retain new drivers, they will enjoy unparalleled pricing power. Truck drivers will also be the biggest winners (which is great). They will take home a lot more pay and will be able to pressure carriers, shippers and brokers that have unfair practices to clean up their act. We can all celebrate that.

Interested in getting an edge on your competitors? FreightWaves is the nerve center of the global supply chain and SONAR is the global dashboard. The SONAR data platform offers the fastest and deepest set of freight market data on the planet. Benchmark, analyze, monitor and forecast everything that is happening around the logistics world with SONAR.