Rejection rates’ continued rise supports the view that a carriers’ market is upon us

This week’s SONAR Pricing Power Index (PPI): 60 (+ 5) – While it’s clear that a major part of the surge in freight data during the past two weeks has been driven by Winter Storm Fern, arguably the most disruptive storm in five years, the magnitude of the movements in freight data, and fact that they have been slow to normalize, give credence to the view that a turn towards a carriers’ market is upon us. Tender rejection rates and spot rates are still likely to decline in the coming weeks as the impact of weather subsides, but they may also stay above the comparable seasonal levels we’ve seen during the past three years.

Three-month SONAR Pricing Power Index (PPI) Outlook: 60 (Unchanged) – Largely due to factors limiting freight capacity, the freight market outlook is to be in carriers’ favor, on a normalized basis (absent weather), in three months. The primary risk to that outlook is uncertain demand, which includes headwinds in the industrial economy and consumer affordability concerns.

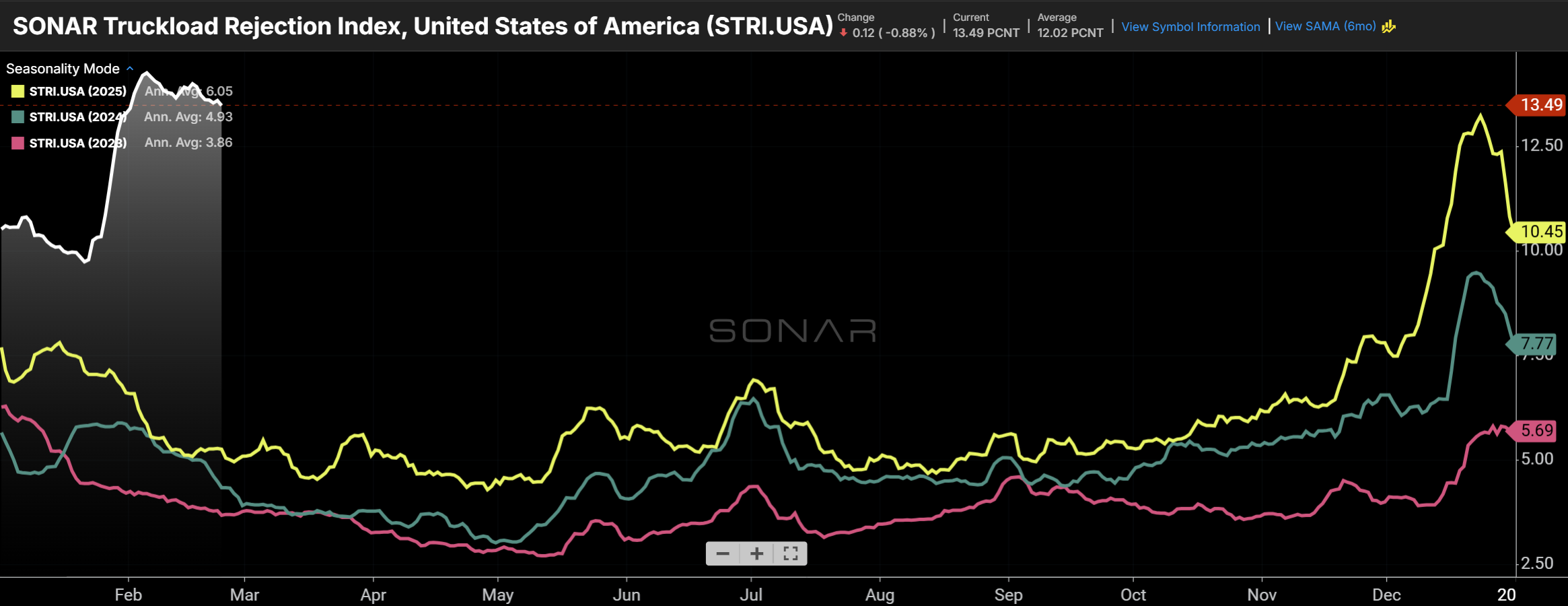

Tender rejection rates keep rising

The national tender rejection rate (2026 – white line) continued to rise this past week and is higher now than at any point in the past three and a half years. (Chart: SONAR)

Certainly, the spike in the national tender rejection rate is being largely driven by Winter Storm Fern, and subsequent storms on the East Coast; the storms have combined to be one of the biggest events to temporarily limit freight capacity in recent years. The disruptive impact extended far beyond the impacted areas as tender rejection rates rose in nearly all of SONAR’s 135 discrete U.S. market segments. The challenge is separating the impact of weather from other market conditions. It will be clear soon enough, even if most of the country really does have six more weeks of winter.

The latest freight market data demonstrates that it is tight enough to make it highly sensitive to disruptive events. That is a trend that analysts at SONAR have been describing all of last year, as rates reacted more sharply to holidays and other events like International Roadcheck than they had in the prior few years.

The latest national tender rejection rate, which reflects carriers’ response to shippers’ requests to move loads during the past week, is currently 14.3%, up from 9.8% before Winter Storm Fern’s impact. For comparison, following the February 2021 Texas Freeze, under the backdrop of an already-tight freight market, the national tender rejection rate increased from 20% to 27%.

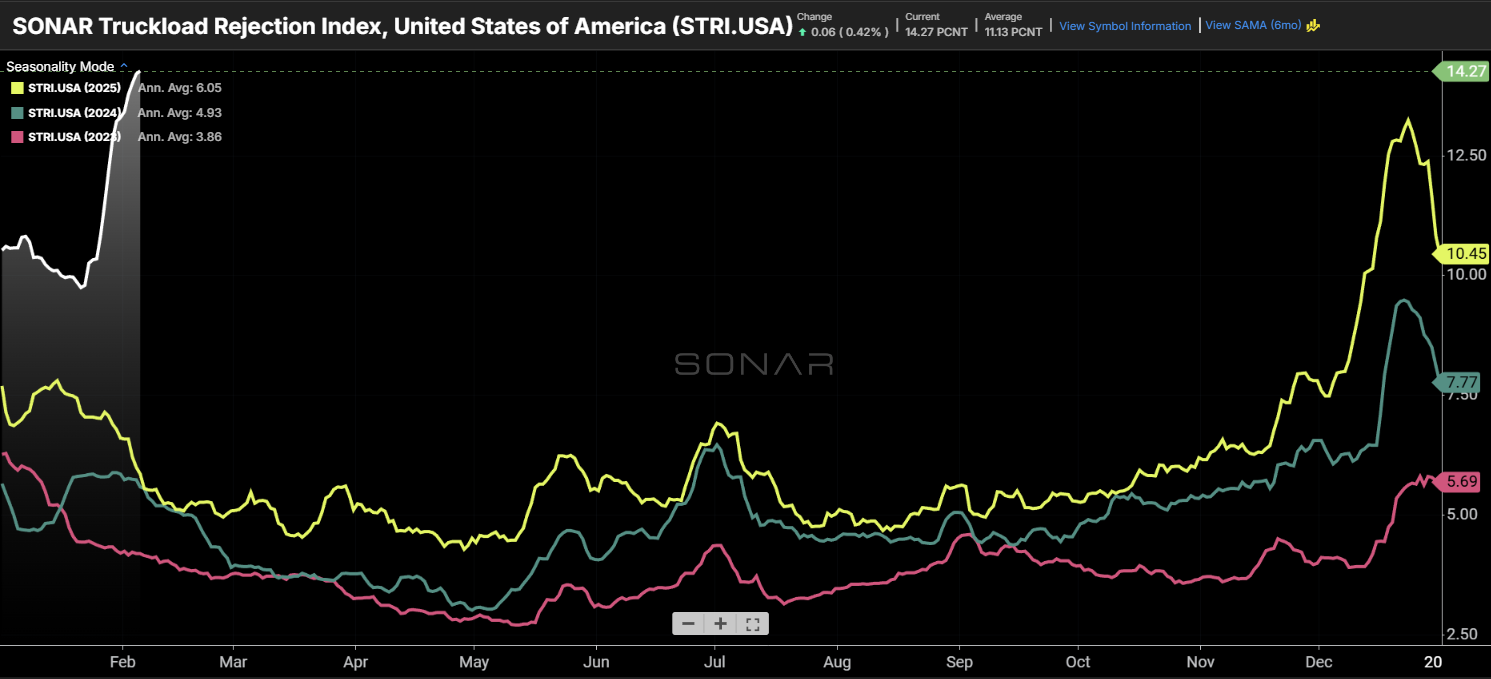

Tender rejection rates have risen across equipment types, with the highest rejection rates in the smaller and more specialized reefer and flatbed segments. The SONAR Truckload Rejection Index is shown above for dry van (white), reefer (green), and flatbed (red) segments. (Chart: SONAR)

How did the storms impact demand?

The SONAR Truckload Volume Index broke out ahead of levels of the past two Februarys. (Chart: SONAR)

Clearly, there’s been a pickup in demand. The question there is also whether it is temporary and caused by the winter storms. It appears that some shippers attempted to move freight early ahead of winter storms. Also, many facilities were shuttered during storms, which, presumably, caused many shippers to get behind schedule, leading to a subsequent surge in requests to move loads.

Total tender volumes increased 4% week over week, in the past week, across all semi-trailer types, and are 7% above year-ago levels. It’s been over a year since SONAR data showed tenders ahead of year-ago levels.

Comparing volume data across modes suggests that truckload may have temporarily taken share from rail intermodal as weather conditions made some shipments more urgent and created downtime at rail terminals. But the latest domestic intermodal volume data, and comments from Union Pacific on its fourth quarter analyst call, indicate that intermodal networks have recovered quickly.

Setting aside the storms, it’s not clear whether demand will be sustainable at above year-ago levels once the impact passes. Prior to the dates impacted by the storm, tender volume had been down about 4% year over year, and down about 6% on a two-year stack. Forward-looking demand metrics are mixed; for instance, the Class I railroads have called out the numerous headwinds they see in the industrial economy, while others point to consumer resiliance, which unusually large tax refunds may bolster.

Domestic intermodal volume dipped during the storm, which may have sent some time-sensitive loads to truckload, but domestic intermodal volume has since recovered. (Chart: SONAR)

Spot rates also surge

The average spot rate, displayed in the SONAR National Truckload Index (NTI.USA), surged following Winter Storm Fern, encouraging carriers to reject tenders. (Chart: SONAR)

Some carriers opt to continue accepting loads during adverse conditions, recognizing that shippers will accept slower service levels. But a coinciding rise in spot rates provided carriers with an incentive to chase more lucrative on-demand loads. The national average spot rate jumped from around $2.55/mile before the storm to $2.82/mile, which was ahead of the Christmas peak of $2.76/mile.

Rising spot rates have led to a collapse in the spread between contract and spot rates. That leads to pressure on brokers’ margins and ultimately, to contract rates priced at higher levels as contracts are rebid. (Chart: SONAR)

About the SONAR PPI: The SONAR Pricing Power Index is a qualitative assessment of the balance of negotiating power between shippers and carriers on a scale of 0 to 100 using SONAR data and anecdotes from discussions with SONAR clients. The higher the number, the tighter the freight market and the more that pricing power favors carriers. A 50 represents a balanced market. While the SONAR PPI primarily pertains to the truckload sector, given its size, dynamics in other sectors, such as intermodal and ocean, are also considered.